ANALYSIS: Dem mega-donor and FTX crypto founder ARRESTED, charged with conspiracy, wire fraud, campaign finance violations and money laundering

12/13/2022 / By Mike Adams

FTX founder and serial liar Sam Bankman-Fried has been arrested by Bahamian authorities under a joint operation with the Southern District of New York (SDNY) U.S. District Court in Manhattan which has leveled multiple criminal charges against Bankman-Fried. He is expected to be extradited quickly to face prosecution in the United States.

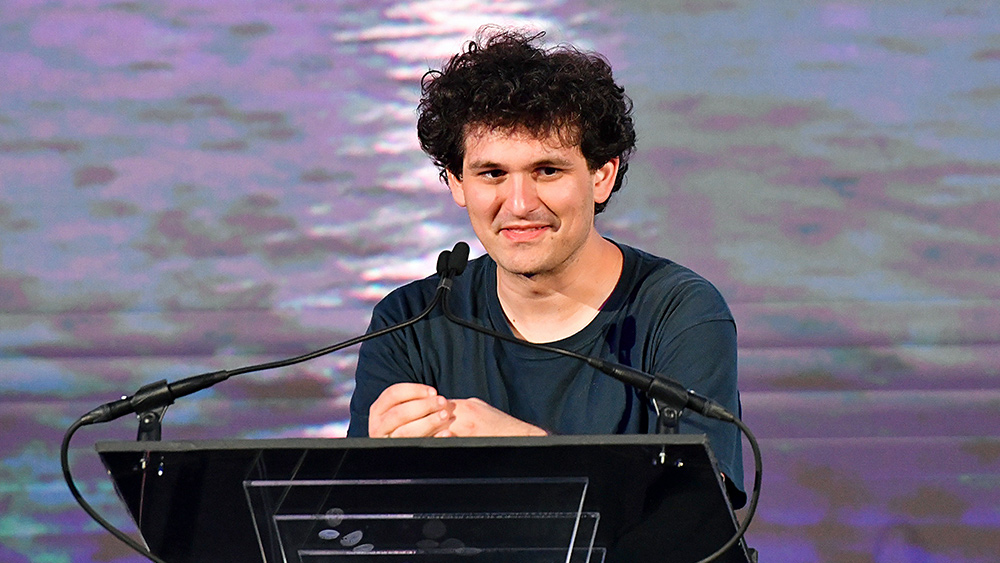

Those charges were unsealed today and reveal that SBF is facing wire fraud, securities fraud, money laundering and campaign finance violations, reports CNBC: (emphasis ours)

Prosecutors allege in the indictment that the former billionaire was engaging in criminal activity that began as far back as 2019 and continued through last month.

Bankman-Fried deliberately and knowingly “agreed with others to defraud customers of FTX.com by misappropriating those customers’ deposits and using those deposits to pay expenses and debts of Alameda Research,” the indictment alleges.

It also accuses Bankman-Fried of conspiring with others to defraud FTX’s lenders “by providing false and misleading information to those lenders regarding Alameda Research’s financial condition.”

Prosecutors also allege he conspired with others to make illegal donations to political candidates, using the names of other persons to mask and augment political giving.

SBF was the second largest individual donor to Democrats in the 2022 campaign, right behind George Soros. The bankruptcy of FTX and the criminal charges now leveled have shut down a slush fund money operation that primarily benefited Democrats and was instrumental in funding the campaigns of Katie Hobbs, John Fetterman and others. (GOP Senate Minority Leader Mitch McConnell, meanwhile, withdrew funding from Blake Masters in Arizona, in an apparent effort to de-fund all “America First” candidates.)

SEC files criminal charges against Sam Bankman-Fried for defrauding investors

In addition to the criminal charges leveled by the SDNY, the SEC has charged SBF with multiple securities violations. According to the SEC.gov press release: (emphasis ours)

The Securities and Exchange Commission today charged Samuel Bankman-Fried with orchestrating a scheme to defraud equity investors in FTX Trading Ltd. (FTX), the crypto trading platform of which he was the CEO and co-founder.

According to the SEC’s complaint, since at least May 2019, FTX, based in The Bahamas, raised more than $1.8 billion from equity investors, including approximately $1.1 billion from approximately 90 U.S.-based investors.

The complaint alleges that, in reality, Bankman-Fried orchestrated a years-long fraud to conceal from FTX’s investors (1) the undisclosed diversion of FTX customers’ funds to Alameda Research LLC, his privately-held crypto hedge fund; (2) the undisclosed special treatment afforded to Alameda on the FTX platform, including providing Alameda with a virtually unlimited “line of credit” funded by the platform’s customers and exempting Alameda from certain key FTX risk mitigation measures; and (3) undisclosed risk stemming from FTX’s exposure to Alameda’s significant holdings of overvalued, illiquid assets such as FTX-affiliated tokens. The complaint further alleges that Bankman-Fried used commingled FTX customers’ funds at Alameda to make undisclosed venture investments, lavish real estate purchases, and large political donations.

Just two months ago, Sam Bankman-Fried was celebrated by the corporate media as a genius, revolutionary figure in finance. He was dubbed the “JP Morgan” of crypto by hosts on CNBC, for example, and over a dozen venture capital firms couldn’t stop gushing over his supposed brilliance, which was apparently indicated by his inability to speak in complete sentences without peppering them with the word, “like.” As in, like, because, you know, like, it was like, never co-mingling, like, customer funds.

To those of us over the age of 30, this speech pattern is only indicative of being a woke idiot. But to woke idiots, it’s a dog whistle for blind obedience and conformity. They are attracted to it like slobbering dogs.

The CFTC also sues FTX founder over fraud

As CoinDesk is now reporting, the CFTC (Commodity Futures Trading Commission) is also suing SBF over allegations that he made “misleading statements” about FTX which caused a “significant price impact” on bitcoin and ether, among other crypto coins. As CoinDesk reports:

“The use of customer funds by Alameda was not authorized by FTX customers, and FTX customers were not made aware that their funds were being used by Alameda,” the filing said, adding that this contradicts both best practices for derivatives exchanges and contractual terms of service.

From the CFTC official press release:

The complaint charges all three defendants with fraud and material misrepresentations in connection with the sale of digital commodities in interstate commerce. Further, the complaint asserts that defendants’ actions caused the loss of over $8 billion in FTX customer deposits.

The complaint alleges that from at least May 2019 through November 11, 2022, Bankman-Fried controlled both FTX.com, a centralized digital asset derivative platform, and Alameda, a digital asset trading firm that operated as a primary market maker on FTX.

In other words, SBF is facing a whirlwind of both criminal and civil penalties, fines, sanctions and very likely prison time if convicted.

Crypto auditors exposed as total junk

Anther big takeaway from today’s events is that crypto auditors appear to be nothing more than rubber stamp firms that fail to conduct serious investigations into the cash and asset flows of crypto companies. As The Gateway Pundit reports:

The auditors of FTX appear to have some serious problems. National accounting firms Armanino and Prager Metis failed to document the FTX multi-billion loans to Alameda in the audited financial statements. They also missed related party transactions with FTX Executives. Massive audit failure.

When the house of cards was collapsing, key players at FTX took out personal loans. Sam Bankman-Fried received a whopping $1.3 billion loan, and other executives received over half a billion dollars in loans. Investigators do not yet know where this money went, and the indictment does not mention how much money was funneled to corrupt politicians as part of the election slush fund / racketeering operations.

ANALYSIS: Federal agencies will leverage the FTX collapse to roll out onerous new regulations on crypto

Sam Bankman-Fried isn’t the only one to blame in all this, by the way. All the people who blindly turned over their money to this woke idiot must also share some of the blame. As is often the case in the crypto space, people just blindly followed the herd off the cliff, conducting zero due diligence to determine whether FTX was really as safe as it claimed to be.

Anyone holding crypto who isn’t right now exiting online exchanges is practically admitting they have no business owning crypto at all. The entire ecosystem was supposed to be decentralized and personally controlled with local wallets. Yet somehow, lured by the promise of impossibly large returns for “staking” coins on exchanges, millions of crypto users put their blind faith in centralized ownership and control. Many of those users have now learned a very difficult and expensive lesson: If you can’t touch it, you don’t own it. (The same rule applies to gold and silver, by the way.)

Or as it is translated in the crypto world: Not your keys, not your crypto.

The sudden aggressiveness of federal agencies in this matter reveals what’s coming next for the crypto industry as a whole: Massive regulation. First, the SEC likely officially declare that all crypto tokens are “securities.” This has been implied but not yet clearly declared in SEC regulations. Next, federal regulators will require crypto platforms to adhere to banking requirements on asset deposits, audits and customer activity monitoring (far beyond today’s KYC rules).

But ultimately, the real nightmare scenario that’s could crater this entire scenario is the U.S. government outlawing private crypto as it rolls out its own Central Bank Digital Currency system (CBDC). After all, governments hate competition, and the easiest way to eliminate it is to outlaw it. Short of outright banning private crypto, the government may attempt to regulate it into obscurity, making it extremely difficult and painful for consumers to use. Should the government succeed in this effort, the value of bitcoin approaches zero.

But an alternative outcome sees the CBDC effort failing and the dollar collapsing as the current world reserve currency (due to BRICS+ nations like China preparing to launch their own gold-backed reserve currency system). In this scenario, crypto may see a resurgence of popularity as people flee fiat currencies and desperately try to buy safety. Physical gold and silver will be “unobtainium” at that point, with no supply available, so many people may attempt to stash cash into something that isn’t collapsing as quickly as the dollar itself. For many people, that could be crypto, which has the advantage of near-instant international settlement capabilities.

Crypto, in other words, has high transactional utility but very low systemic trust. The best way to use crypto is to get in, conduct a transaction and get out as quickly as possible, minimizing counterparty risk.

Despite users’ best efforts, however, crypto will always be subject to high counter-party risk. As we’ve all seen with FTX, crypto exchanges can vanish overnight, taking billions of dollars in customer assets with them. Crypto scams and frauds have extensively proliferated over the last five years or so, causing many would-be users or investors — especially institutional investors — to wash their hands of it and look elsewhere. Thanks to SBF and FTX, the crypto space is increasingly becoming synonymous with Ponzi schemes, con artists and fraud. This reputation was in effect “earned” by the crypto community, given how many crypto YouTubers were pumping FTX in exchange for affiliate commissions. Even Tom Brady was ensnared in the scheme as a spokesperson for FTX.

We anticipate lawsuits against prominent FTX-pimping Youtubers who earned millions of dollars pushing the FTX fraud. Some have already begun to flush their entire Youtube channels in the hope that they might escape further scrutiny. But the internet remembers everything, and these efforts will likely not succeed.

Crypto will now go through a devastating detox phase

The bottom line is that crypto is about to endure a very dark DETOX phase in which scammers, fraudsters and hype artists are going to be cleaned out, wiped out and in some cases imprisoned. Onerous new regulation will be inflicted upon the industry, erasing most of the supposed “benefits” that crypto users previously enjoyed through schemes like “yield farming.” With heavy regulation, there are fewer reasons for people to buy and hold crypto, and the entire “hodler” argument unravels quickly. When the hodlers stop hoddling, the speculative hype no longer works, and crypto collapses to what it was mostly meant for in the first place: A utilitarian asset used for transferring funds or clearing transactions, but not a speculative investment and definitely not “digital gold” (that argument was always premised on failed logic from the very start).

The good news is that crypto does have a future as a transaction settlement system that’s heavily regulated and no longer speculative. This will make crypto boring and useful, which is exactly what it needs to be to gain long-term acceptance. Whether private crypto will be outlawed in the United States is a debatable issue, but it is not debatable that the footloose haphazard “anything goes” era of crypto is rapidly coming to an end. And this is good for crypto in the long run, since the scammers, fraudsters and con artists were inevitably going to be destructive to the entire ecosystem. Better to root them out now than to let them dominate the space and turn the entire system into a digital mafia operation. (Because that’s the job of the Federal Reserve, of course.)

I cover all this and more in today’s Situation Update podcast:

– Sam Bankman-Fried charged with wire fraud, conspiracy, money laundering

– Looks like paying off Democrats didn’t achieve criminal immunity after all

– Twitter accused of being run by “gay mafia” of enforcers

– They SILENCED conservatives but did nothing to stop child exploitation

– Twitter was a child trafficking, grooming, pedo CESSPOOL run by Leftists

– CNN producer pleads guilty to child exploitation, groomed 7-year-olds in his ski lodge

– WEF calls for ending private car ownership

– Ed Dowd’s new book launched, “Cause Unknown”

– Pope Francis says no one should have relationship with Christ

– Chinese police arrest TETHER (stablecoin) money laundering gang

Brighteon: Brighteon.com/877e7fb4-b3da-4e15-925c-9604ab190df8

Rumble: Rumble.com/v20e5te-situation-update-dec-13-2022-ftx-crypto-founder-arrested….html

Bitchute: Bitchute.com/video/iZQEBQMsTp9E/

Banned.Video: Banned.video/watch?id=63984d543454fe1dfa89504d

iTunes podcast: Healthrangerreport.com/situation-update-dec-13-2022-ftx-crypto-founder-arrested-twitter-was-run-by-pedo-pushing-gay-mafia-enforcers

Discover more interviews and podcasts each day at:

https://www.brighteon.com/channels/HRreport

Follow me on:

Brighteon.social: Brighteon.social/@HealthRanger (my breaking news gets posted here first)

Telegram: t.me/RealHealthRanger (breaking news is posted here second)

Substack: HealthRanger.substack.com

Banned.video: Banned.video/channel/mike-adams

Truth Social: https://truthsocial.com/@healthranger

Twitter: @MikeAdamsHR

Gettr: GETTR.com/user/healthranger

Parler: Parler.com/user/HealthRanger

Rumble: Rumble.com/c/HealthRangerReport

BitChute: Bitchute.com/channel/9EB8glubb0Ns/

Clouthub: app.clouthub.com/#/users/u/naturalnews/posts

Join the free NaturalNews.com email newsletter to stay alerted about breaking news each day.

Download my current audio books — including Ghost World, Survival Nutrition, The Global Reset Survival Guide and The Contagious Mind — at:

https://Audiobooks.NaturalNews.com/

Download my new audio book, “Resilient Prepping” at ResilientPrepping.com – it teaches you how to survive the total collapse of civilization and the loss of both the power grid and combustion engines.

Submit a correction >>

Tagged Under:

banned, Big Tech, censored, Censorship, conspiracy, crypto, finance, fraud, free speech, freedom, FTX, gay mafia, Glitch, left cult, LGBT, Liberty, money, ponzi, risk, Sam Bankman-Fried, scam, tech giants, Twitter, Tyranny

This article may contain statements that reflect the opinion of the author

RECENT NEWS & ARTICLES